Apply For An IVA And Write Off Up To 85% Of Your Unaffordable Debt

- Stop Creditor Calls

- Freeze Interest and Charges

- Free, No Obligation Consultation

- Discover The Right Solution For You

May not be suitable in all circumstances. Fees may apply, read here. Entering into a Protected Trust Deed may affect your credit rating.

What Is An IVA?

An IVA can be a great, positive way to help with your debt. Allowing you to continue living your life without the stress of being chased by your creditors.

An Individual Voluntary Arrangement (IVA) is a debt solution where you agree with your creditors to pay all or part of your debts. This agreement is set up and managed by an Insolvency Practitioner (IP), who will receive an agreed monthly payment from you and will divide it amongst your creditors.

if you apply for an IVA, then this agreement could allow you to write off up to 85% of your total debt based on government legislation and will often give you a greater level of control than bankruptcy.

Once your IVA has been agreed and set up, your creditors can no longer take action against you and won’t be able to contact you, but it will affect your credit rating for six years, making it difficult to get further credit during this period. Your details will also be placed on The Register of Insolvencies, which is a public record, while you clear your debts.

For the duration of your IVA, all fees and interest relating to your debt is frozen and once completed, the remainder of your debt is written off, allowing you to begin again, debt free.

This agreement is available to residents of England, Wales and Northern Ireland. If you live in Scotland, then you could pursue an agreement called a Trust Deed to help you with your debt.

- You Have Over £7,000 of Debt to Repay

- You Owe to More Than One Creditor

- Live in England, Wales or Northern Ireland

- You Have a Regular Income

If you fit the above criteria, then there is a high likelihood that you will qualify for an IVA. If your individual circumstances are different, for example, you live in Scotland or your debt is slightly lower than £7,000 then enquire with us anyway; we could still help.

Credit Cards

Unsecured Loans

Store Cards

Overdrafts

Personal Loans

Utility Bills

Business Debts

Catalogues

Debt Collectors

Bailiffs

Whether it is a Trust Deed, Sequestration or a Debt Arrangement Scheme, only unsecured debt can be included in a debt solution.

Here are some examples of some typical unsecured debts that you may have.

Self Employed IVAs

IVAs for the self-employed work in a very similar way to a typical IVA, where an Insolvency Practitioner will arrange and agreement of monthly payments that you can afford. There are, however, a few differences.

- Self-Employed IVAs can often be arranged in a way that allows for greater flexibility across a year. This can be good news for businesses that rely on seasonal income. A cash flow statement will need to be produced so the IP can understand your business and what you can afford.

- If your business relies on Business Credit to operate during the term of the IVA, then this can be pre-agreed with your creditors. You creditors may have specific criteria that they will require you to follow to maintain the agreement.

- A business may need ongoing trade with one of the creditors it has fallen into arrears with. Under these circumstances, certain Trade Creditors may be excluded from the IVA agreement, so as not to affect future business relations.

Joint IVAs

Couples with a combination of individual and joint debts can set up individual IVAs which include all their debt however, once these are agreed, they can be administered jointly, allowing the couple to pay one affordable monthly payment.

Full and Final IVAs

This can be a great option for those who want to make a one-off payment to creditors as a final settlement

This can be an appropriate option for those with adequate savings or those who are in the process of receiving sufficient funds due to the sale an asset.

This can also be an option for those with friends or family whoa are prepared to provide the funds to cover the total amount of the IVA.

Remember, if you are struggling with debt, you are not alone. Contact us at Apply For An IVA to take the first step towards a debt free life.

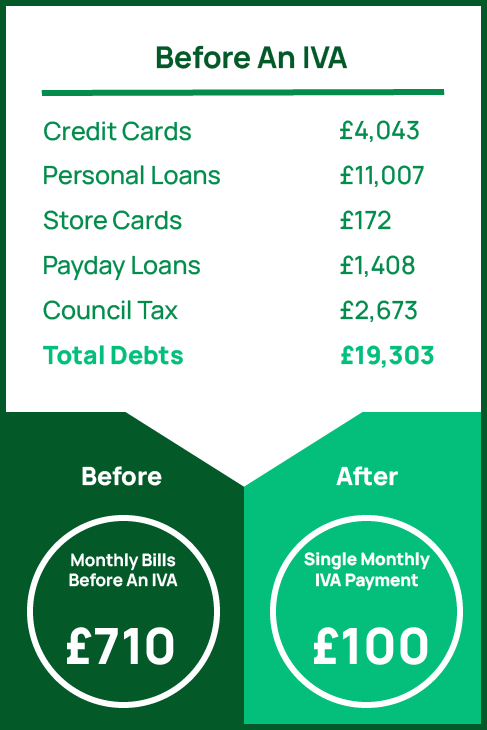

This is a real life example of how we have helped one of our customers. Enquire Today.

IVA Application

We strive to ensure that when you apply for an IVA, it is as pain and fuss free as possible. Take a look at how an IVA application works.

1.

Speak To An Advisor

Signing up to a debt solution is a significant event in your life, so it is important to gather as much information as possible, so you can make an informed decision as applying for an IVA is not your only option.

While researching your options before you register or sign up, you may find our articles on IVAs and how they work.

Once you feel ready, fill in our form and a member of our IVA team will contact you.

Our experienced advisors will be able to guide you through your options discovering which one best applies to you, ensuring that, even if we cannot help you ourselves, we can point you in the right direction of help appropriate to your personal circumstances.

In order to determine which course of action is right for you, we will discuss your debt. This will involve how many debts your have, who you owe money to and how much you owe to each business. If you are not sure about the details of your debt then we could always run a credit check for you.

2.

Send In Your Documents

During the IVA application process, there are several documents that we will request.

We will ask you to provide:

- Photo ID

- Rent Agreement or Mortgage Statement

- Latest 3 Months of wage slips

- Latest 3 months of bank statements

- Council Tax and Utility bills

- HP agreement if appropriate

- Recent statements from any other creditors you may have.

Which information you are asked for will largely depend on your personal circumstances and as such, the above list is to be used purely as a guide.

There will also be a discussion regarding your other living expenses and how you spend your money, such as food bills and travel expenses. This allows your advisor to determine your affordability, ensuring you don’t sign up to an IVA that isn’t appropriate for you, it is important that the rules and regulations are met. It would not be great to learn at a later date that an IVA solution for your debts and finances wasn’t the best option.

3.

IVA Drafter

Once all of the information has been gathered, your IVA advisor will book you in for a SIP (Statement of Insolvency Practice). This is a mandatory legal procedure that all debt management companies MUST follow and must be recorded. It exists to ensure that you and your debt are handled in accordance with the law and that all compliance standards have been met. This procedure reconfirms that the IVA is in your best interests and that you have been made aware of any alternative solutions.

Once the SIP has been completed, your Drafter will then ‘draft’ your IVA. This means that they will raise the legal documentation.

The Drafter will check through the information you have provided and will ensure that everything is in order to successfully proceed with your proposal, including making sure that all evidence of your circumstances are available should your creditors request more details. You will then be sent a copy of your proposal to sign.

4.

Meeting of Creditors (MOC)

The Meeting of Creditors (MOC) is the process by which your creditors vote in favour of, or against your IVA proposal.

It isn’t an actual meeting, but instead refers to a period of time in which your creditors can to respond to the proposal. All of the creditors included in the IVA are entitled to vote, however they do not have to.

In fact, some creditors will have a policy of either automatically accepting or rejecting an IVA, considering each case individually or a policy of never voting at all. Rest assured though, that all debt management companies have a high degree of awareness as to how each creditor behaves and it is highly unlikely that your application would get this far unless they were confident that you would succeed.

Here are the rules for MOC in a little more detail:

On applying for an IVA, your debt will be analysed to see who your creditors are and how they typically vote. A successful application must have the following:

- A minimum of one positive vote, therefore at least one of your creditors must either have a policy of voting positively or to at least consider IVAs and then go on to vote for your IVA.

- 75% of the ‘voting creditors’ must vote positively, or the positive voters must represent 75% of the total voting debt amount.

This basically means that when deciding whether you qualify for an IVA, only the creditors that vote affect your outcome. You could owe a total of £50,000 across 10 creditors, but if only one votes at all and they vote positively even if you only owe them a small amount, then the IVA would go through and the other creditors would be legally obliged to follow it.

5.

A Successful Application

If your application is successful, then you will be passed over to an IVA Supervisor who will take your card details in order to set up a recurring card payment. This is the typical method for making your monthly payment towards your IVA.

After this, you will be contacted each year of your 5 or 6 year IVA period to discuss how things are going and to make any adjustments to the IVA should your circumstances have changed.

What Are The Pros and Cons Of An IVA?

Pros

During the application process, you will be given a copy of your agreement, clearly stating your fees. All fees are covered by the monthly payment you make, so you will never be asked to pay anything up front or at the end of the IVA period.

By agreeing to your IVA, your creditors are also agreeing to cease any action they may be taking against you, leaving you in peace.

Your creditors will literally vote for or against your IVA proposal. If the majority say yes, then the rest of your creditors are legally bound to follow.

While your IVA live, your creditors can not add any fees or interest to the balance. However, it is worth noting, that should your IVA fail, perhaps as a result of you not keeping up with repayments, then charges and interest can be applied from that point forward.

As part of the application process, your Insolvency Practitioner will judge how much you can afford a month towards your debt. You will have the opportunity to discuss all of your incomings and outgoings so we can find the best solution for you.

If you circumstances change for the worse, then as long as you are honest and open about this, you may be able to take advantage of some payment holidays, or to have the IVA adjusted.

Once your IVA period has ended, any debts that were agreed in the IVA at the beginning that still have an outstanding balance, will be written off.

An IVA should not put your home at risk. If you have a mortgage then this will not be able to be included in an IVA, so as long as you can keep up with your repayments as normal, your home is safe.

Cons

Your Insolvency Practitioner will only be able to include unsecured debt into the agreement.

When presented with your IVA Proposal, your creditors will be asked to vote on whether they think it should go ahead. Occasionally, you may lose this vote.

If your mortgage has a fixed rate, then at some point during your IVA, you will likely need to remortgage your property. At this stage you could be asked to release any equity you have in your property and put it towards your debt.

If you receive funds greater than £500 as a result of inheritance or other such circumstances during the terms of the IVA, then you will need to inform your IP who may want to take a portion of it to put towards your debt.

If this happens, then your creditors will be able to begin chasing your arrears again, potentially adding interest and charges.

If your creditors refuse to comply with this, then your IVA could fail.

This is a public record, so anyone looking for this information could potentially find your details.

This is a negative, but if you have missed payments on your debt already, your rating could already be low. It is also 6 years from the start of your IVA, so once it is completed your IVA should be no more than one year away from your credit score beginning to recover.

If you miss payments and your IVA fails, then your creditors could petition for you to be made bankrupt.

Friendly & Understanding

Our friendly, understanding and expertly trained advisors are ready to assist you, offering impartial and practical guidance in a completely non-judgmental setting. We recognise that anyone can encounter financial challenges, which is why we prioritise treating our customers with empathy and understanding.

Proven Track Record

With over 20 years of experience, we have helped literally thousands of people solve their money worries. Once you have enquired, one of our team members will be in touch, learning about your specific circumstances and pointing you in the direction of the help you need; whether that is with us, or one of our trusted partners.

Ongoing Support

If you choose to become one of our clients then, should you need us, we are here to help. We understand that life can be tough and we can all be faced with the unexpected from time to time, so should your circumstances change during your Trust Deed term, get in touch and get the support you need.

What is an IVA and how does it differ from a deed?

An IVA, or Individual Voluntary Arrangement, is a formal agreement between a debtor and their creditors to pay back debts over a period of time. It differs from a deed in that it is legally binding and involves the supervision of an insolvency practitioner. A deed can refer to any legal document that signifies an agreement or contract, not necessarily related to debt.

How might empathy play a role in the process of applying for an IVA?

Empathy can be important when communicating with creditors during the IVA application process. Demonstrating an understanding of each partys situation may encourage cooperation and facilitate the negotiation of terms that are fair and manageable for both sides.

Can applying for an IVA stop bailiffs from taking action against me?

Yes, once you have applied for an IVA and it has been approved by your creditors, bailiffs are no longer allowed to take action against you. The approval of the IVA legally protects you from any further enforcement actions as long as you comply with its terms.

What happens if my financial situation changes after entering into an IVA?

If your financial situation changes significantly after entering into an IVA, you should immediately inform your insolvency practitioner. They can assess whether your payment plan needs adjusting or if other arrangements should be made within the terms of the existing agreement.

Is there any risk involved in applying for an IVA?

Yes, there are risks associated with applying for an IVA. For instance, if your proposal is rejected by creditors or you fail to keep up with payments once its accepted, this could lead to bankruptcy proceedings. Additionally, IVAs affect credit ratings negatively and will appear on public records such as the Individual Insolvency Register.